During your first six, you will likely have been covered by your pupillage award and any savings you may have had prior to joining the bar.

From your second six, you can accept instructions and are largely responsible for your own earnings. Depending on your set, you may receive a further flat lump sum, or they may guarantee your earnings through a top-up.

This is the time we find barristers begin to ask questions about their finances.

Talk to your peers

First and foremost, we encourage pupils and junior barristers to talk with their more experienced peers. They have been through this before. No one can speak more to that experience than they can.

Many will share tales of their first years in practice, how they dealt with moving into self-employment, how they may have been caught out by the January or July deadline, and they may provide recommendations for accountants they trust.

When we speak to your peers, there are a few common themes we hear:

Get your house in order

Your chambers may encourage you to register for VAT immediately; regardless of whether they do, it is likely to be a good decision to do so, as you will be able to reclaim VAT on major expenses, e.g., business travel and accommodation, and professional subscriptions.

While not required, opening a business current and savings account as you enter practice is prudent. This approach helps segregate finances and can reduce admin and back-and-forth with your accountant at tax year-end.

Now may be a good time to interview accountants to find one who fits you.

When looking for an accountant, it is important to consider:

· Whether they have experience of working with barristers

· Whether how they communicate throughout the year works for you

· How their fees change over the years

Begin by building up some cash reserves

During the first seven years of your practice, you will likely experience a degree of instability when it comes to the volume of work available through the year and the urgency in which you are paid for the work done and while your clerks and practice managers will provide invaluable guidance on hourly rates, when to expect income, and how to chase outstanding fees, the reality of life at the junior Bar is that payment timelines are rarely consistent.

Without a cash buffer, a quiet month or delayed payment can quickly become a genuine source of financial stress.

We suggest building a cash reserve equal to two to three months of essential outgoings. This does not need to happen overnight. Even setting aside a modest, fixed portion of each fee will let you gradually build a buffer. This allows you to focus on your practice, not your bank balance.

Treat your cash reserve as a non-negotiable first allocation when a fee lands. Before discretionary spending, funding your ISA, or pension contributions, ensure your reserve is maintained. Once at your target level, redirect those allocations to longer-term goals.

Think about protection

Nobody enjoys thinking about what happens if they become unwell or have a serious accident and are unable to work. However, it happens, and if you are a self-employed barrister, there is no sick pay or cover provided for you; you would be dependent on any safety net you would have built.

An Income protection policy pays a portion of your income if you can't work. Premiums are usually lower if you're younger and healthier when you apply.

Additional steps you can take for future financial security and flexibility

Once the immediate admin is in order, we’re often asked what additional steps can be taken. There are two additional steps that will reward you significantly in the long run.

We encourage you to open a ‘Flexible’ Individual Savings Account (ISA) if you have not done so. An ISA lets you contribute up to £20,000 and returns grow entirely free of income tax and capital gains tax. You can withdraw from an ISA without penalty (except for a Lifetime ISA). We always recommend ‘flexible’ ISAs, which let you withdraw funds and, if returned within the same tax year, do not affect your ISA allowance.

For those of you with a clear goal of becoming a first-time buyer, it may be worthwhile to explore a Lifetime ISA.

Additionally, if you can, it may be worthwhile to open a personal pension. Many young barristers ignore their pension for several years; however, to make a quick case for the pension:

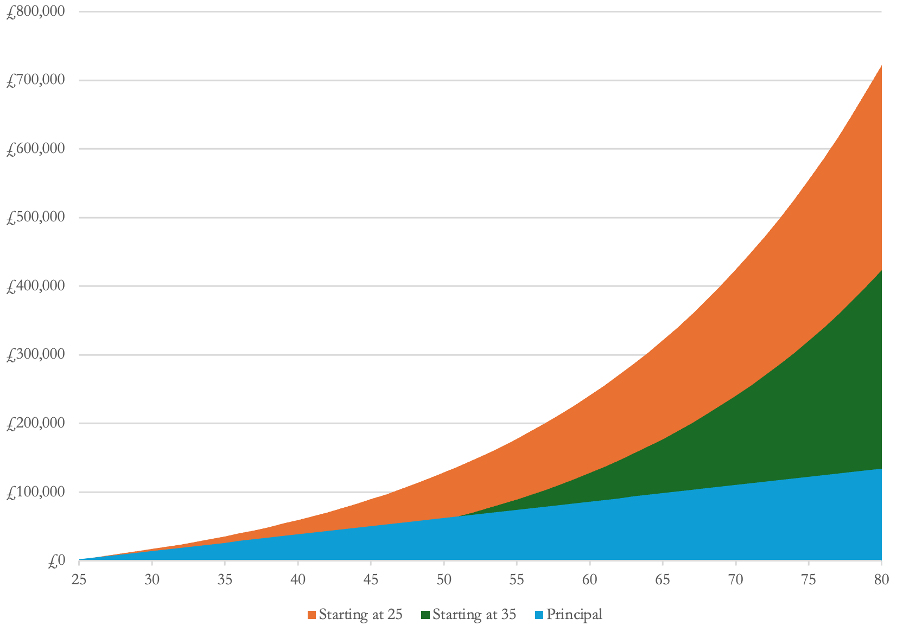

On point 3, compounding is best demonstrated visually.

The graph below shows the long-term impact of investing £200 per calendar month from:

We assume your investments grow at 5% per year, with no withdrawals until age 80.

By age 80, if you started investing at 25, you would be about £300,000 better off than if you started at 35. You would have invested an additional £24,000 in principal (£200 per month for 10 years). By age 80, you will have contributed £134,400 (£200 per month for 55 years).

Consistent 5% annual investment growth without downturns is rare. However, since 1984, the FTSE 100 has averaged about 5.2% per year through 2023.

How We Help at H&H

At Halesworth & Hurlston, we work exclusively with barristers and have supported many going through second six and beyond. We help you understand your finances, build tax-efficient wealth to meet your goals, and develop long-term financial stability that evolves with your career.

If you are seeking clarity on your personal finances or want a professional review of your existing arrangements, don’t hesitate to contact us. Arrange your complimentary, no-obligations consultation today and take the next step toward securing your financial future.

Disclaimer: This article is for informational purposes only. It does not constitute financial advice. We recommend speaking with a qualified financial adviser who knows the needs of self-employed barristers.

If you are ready to work with a financial planner who understands the finer details of life at the Bar.

Some may prefer to manage their own finances but would appreciate guidance on how to do so.

Schedule an introductionLearn about our self-directed courseIf you are ready to work with a financial planner who understands the finer details of life at the Bar

Schedule an introductionIf you would prefer to see how we have supported barristers in similiar situations to you

Learn more